Inflation outlook and foodservice market update - January 2026

16 January, 2026

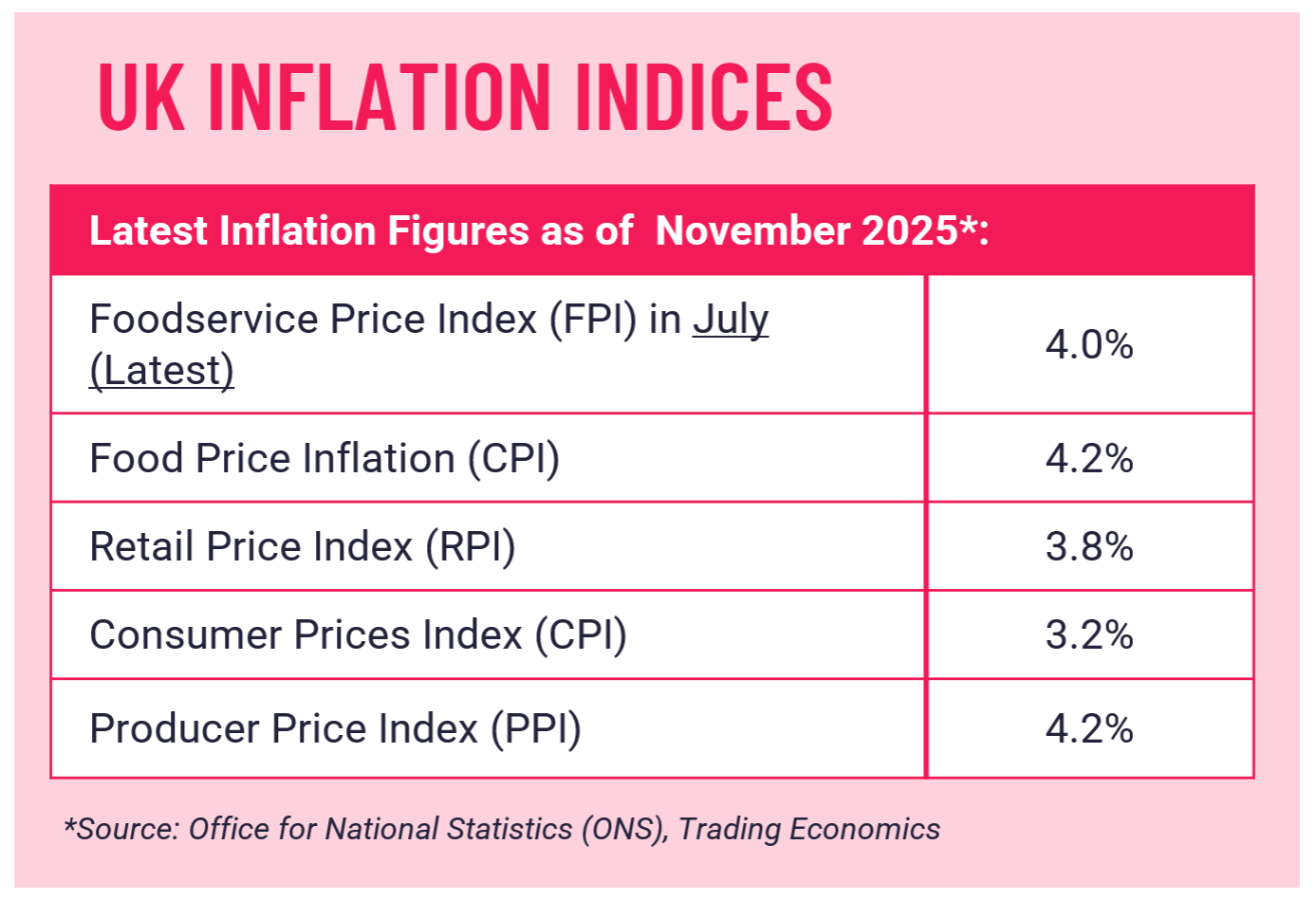

The Consumer Prices Index Headline Rate (CPI) rose by 3.2% in the 12 months to November 2025, down from 3.6% in the 12 months to October. Food inflation remained higher than the headline CPI rate at 4.2%, although down from 4.9% in October. The main driver of the monthly inflation slowdown was breads and cereals and to a lesser extent dairy products and the sugar, jam, syrups, chocolate and confectionery class.

Market movers:

FISH & SEAFOOD

Salmon – The market remains firm as winter sets in. Colder water temperatures are slowing growth rates and increasing quality challenges, which in turn limit the supply of larger, premium-size fish. This continues to put pressure across fresh, frozen and smoked salmon. Pricing remained high throughout December as seasonal demand peaked.

Shellfish – Warm-water prawns remain relatively stable, supported by improved farm output, though labour and freight costs are keeping prices from falling. Crab and lobster remain expensive compared with earlier in the year, as weather disruption and strong export demand affect availability, particularly for live product. To manage volatility and maintain menu continuity, we are recommending that operators increase their volumes of processed and frozen formats.

Whitefish – Cod remains under significant pressure, with prices still at multi-year highs. Ongoing quota cuts and tight supply means little relief is expected in the short-term. Haddock, as a natural substitute, has also seen prices rise as demand shifts away from cod.

FRUIT & VEG

Europe – Growers are currently facing challenging conditions as rain and freezing temperatures disrupt harvesting.

Spain – Persistent rain and cold weather continue to affect crop cycles and quality.

UK – A severe cold snap is impacting production, though conditions should improve soon.

North Africa – Morocco is seeing lower-than-expected temperatures, adding pressure to supply.

MEAT

Beef – December saw beef prices dip slightly, driven by sluggish market demand. Overall demand remains stable, but consumers are shifting towards cheaper cuts.

Chicken – Widespread shortages due to Avian Influenza (AI) throughout 2025 have led poultry farmers to increase the number of chickens sent for slaughter. Supply bounced back in December, although caution is still advised, as AI outbreaks are more common during winter months.

Turkey – December saw demand surge over the festive period. Ongoing AI outbreaks in the UK and Europe have reduced flocks and prompted culls, limiting availability. Suppliers are reluctant to commit to fixed prices or volumes this season, pushing prices around 30% higher than this time last year.

GROCERY

Mushy Peas – Harvests have improved this summer in several key growing regions, particularly in North America, for dried marrow fat peas, the main ingredient in mushy peas. As a result, prices have softened, making them an attractive side option for fish & chips.

Quinoa – The market has firmed in recent months as demand has exceeded supply. Exports are up 12% year-on-year. With no leftover stock from 2024, prices started to rise towards the end of the season. The 2025 crop is expected to be 7% smaller than needed to meet demand.

Canned Pulses – Better harvests in summer 2025 in key growing regions, including the US and Canada, have improved availability for chickpeas and red kidney beans. As a result, chefs are increasingly being encouraged to include pulses in recipes as a plant-based source of protein.

UK KEY MARKET MOVERS (CPI)

The Consumer Prices Index (CPI) is a key measure of inflation in the UK. Movements in CPI give a high level overview of the key categories experiencing inflation. Below is a monthly snapshot of the top food commodity price inflation movements impacting the UK. The data is from Office for National Statistics (ONS).

Percentage change over 12 months:

Milk, cheese and eggs: 2.5%

Oils and fats: 0.7%

Breads & cereals: 2%

Vegetables: 2%

Meat: 6.5%

Sugar, jam, syrups, chocolate and confectionery: 11.2%

Fish: -0.3%

Fruit: 2.4%

FINAL WORD

Regency continue to proactively mitigate availability issues and supply risk, putting solutions in place to reduce impact, such as product switches and recipe re-engineering.

When analysing the affects that inflation has on your businesses purchasing, it's important to understand that inflation affects not only the price of goods, but also the quality and availability - this is something that our team of procurement experts can assess in detail, to ensure our members are always achieving the best outcomes in all areas.

Equally, we fully understand the challenges presented by the increase in Employer National Insurance Contributions and National Living Wage, along with reduction in business rates relief and increased water bills. Our team of experts are working closer than ever with our members to reduce their purchasing costs in attempt to lessen the impact of rising costs in other areas of the business.

To find out more about ways in which we can help save your business time and money, get in touch.

Sources: Foodbuy, Fairfax Meadow, Birtwistles.

We use cookies to ensure you get the best experience on our website. Learn more

Stay connected

Enter your email address to be kept up to date with latest news, company developments and market insights. You can unsubscribe at any time.

View our Privacy Policy.