Inflation outlook and foodservice market update - Aug/Sep

3 September, 2024

After a weak end to 2023, where the UK fell into a brief recession, economic data in 2024 has been more positive. The Office for National Statistics (ONS) has reported that the economy grew by 0.7% in the first quarter of the year and 0.6% in Q2.

The BoE has now acted to address this issue as inflation levels have reduced, cutting interest rates in August from 5.25% to 5%. It has however been cautious, citing the lack of reduction in services inflation, which remains well above long-term averages, as the primary reason.

Services inflation is predominantly driven by wage growth, and policymakers want to ensure that this is under control before loosening their grip on monetary policy more materially.

Forecasts for future economic performance and inflation currently show a changeable landscape. After falling to 2% in June, top-line inflation rose to 2.2% in July. A key factor in the decline of inflation in 2023 and 2024 has been falling energy prices. The chart from the Bank of England illustrates this, showing that inflation would be closer to 4% currently if energy were removed from the calculation.

Going forward, as the price reductions in the energy sector inevitably slow and come to an end the BoE forecasts that inflation will rise to 2.7% to end the year.

Looking at food prices in isolation, a similar shape is observed. The lack of material cost reductions in the manufacturing sector and continued cost pressure from wages have led forecasters to predict that food inflation will rise in the second half of 2024.

The Institute of Grocery Distribution (IGD) estimates that the CPI rate for food in the UK will reach a low point of near zero in September before rising to 2% by the end of the year, with that rate of price rise continuing throughout 2025.

Looking longer term, forecasts suggest that both economic growth and inflation will cool off. The impact of prolonged restrictive monetary policy on businesses has likely not fully been observed yet, and the new Labour government is signalling ‘tough decisions’ ahead, which will likely involve a cut in spending. The BoE’s forecast is aligned to this as it predicts that CPI will fall below 2% in 2026.

Food and drink overview

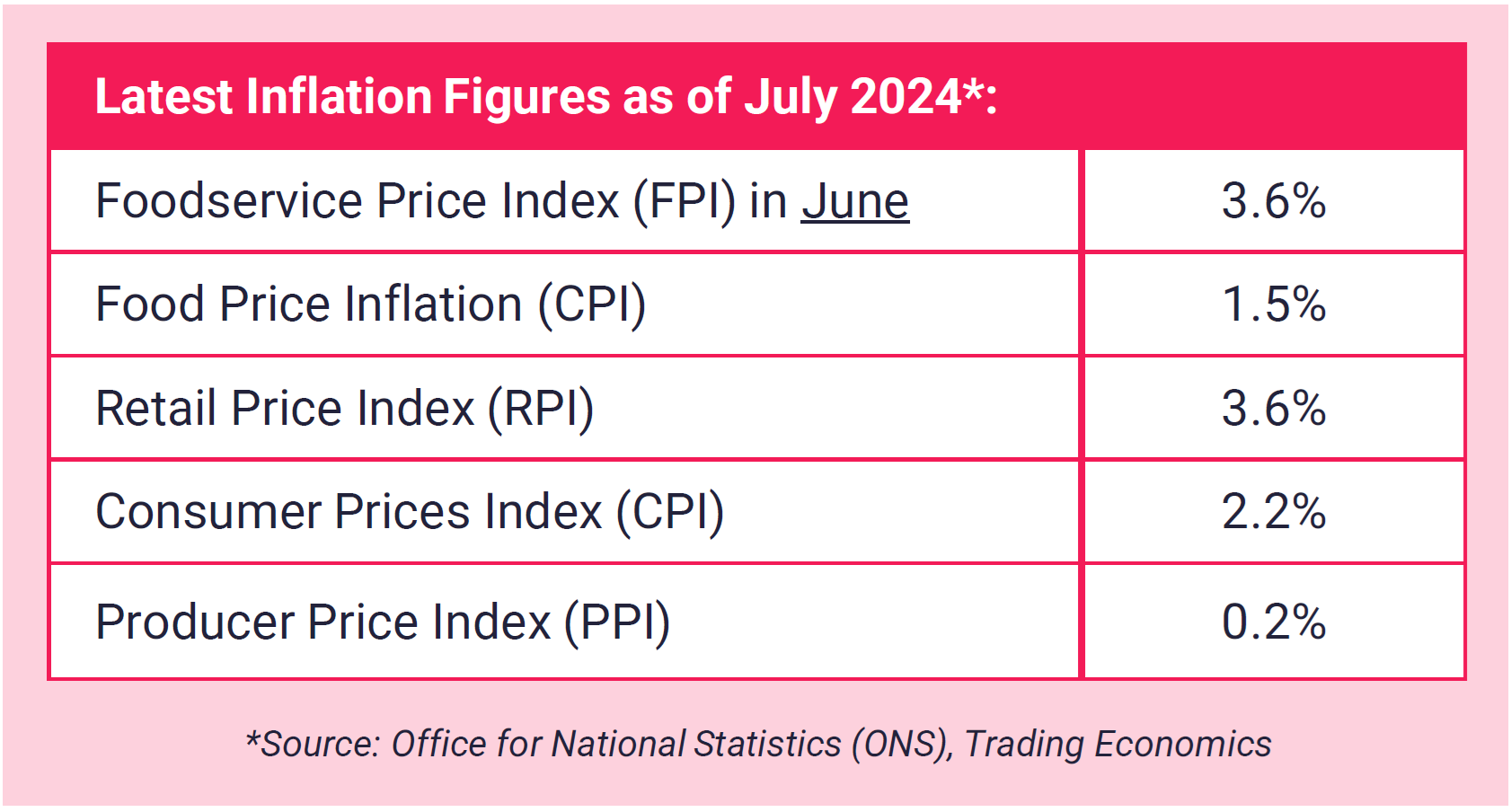

In July 2024, the Consumer Price Index (CPI) increased to 2.2%, reflecting a slight rise in inflation. Food and nonalcoholic beverage prices stabilised, with a 1.5% annual increase, marking a pause in the easing trend seen over the past 15 months. The Retail Price Index (RPI) rose to 3.6%, driven by steady increase in food and catering prices, while the Producer Price Index (PPI) for food saw a modest 0.2% annual increase, after a fall in June.

Market movers:

FISH & SEAFOOD

Prices of farmed Bass and Bream are experiencing a steady monthly increase, primarily due to rising transport costs from Europe. Limited Bream biomass on farms is exerting additional pressure on pricing.

Cod prices are starting to rise as supply tightens, with the last quota’s volume nearing its end. Some relief is anticipated once the new quota is established in September.

The scarcity of farmed Halibut, particularly larger specimens, has resulted in higher prices. Harvesting remains sporadic and this is expected to continue until biomass levels show a reliable increase.

TIP: Mackerel is a great catch this month, with excellent quality and value, but it won’t be in season for long. Looking ahead, British Shellfish will hit peak season from September through the winter, so be sure to include them on your menus in the coming months.

BEEF

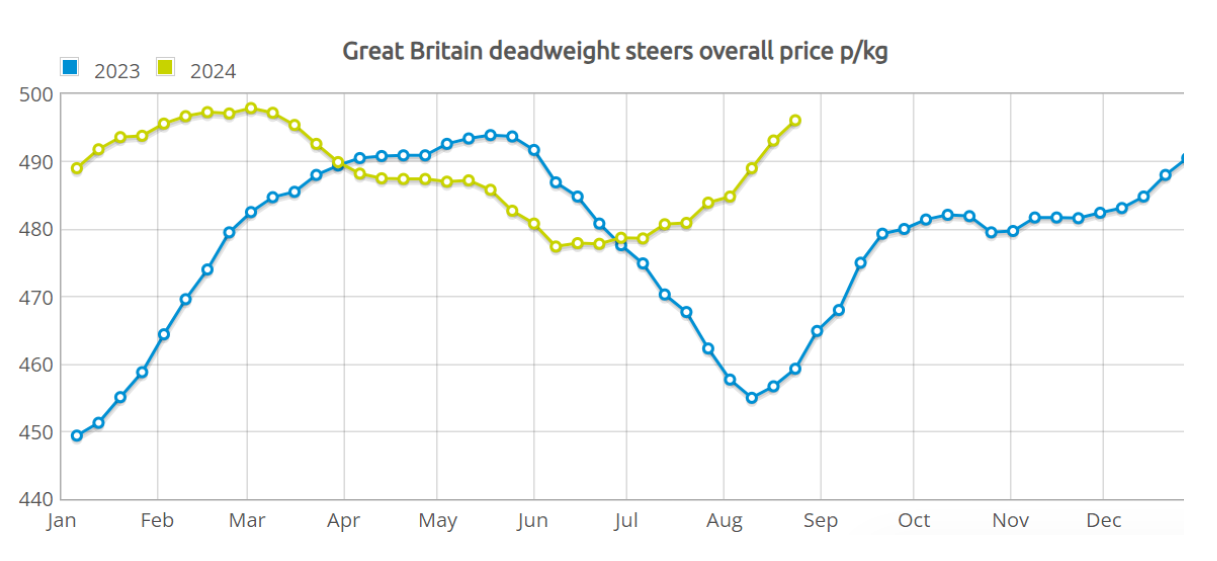

Following heavy periods of rainfall and sunny spells in late July, grass is growing, meaning farmers continue to leave the cattle in the field.

Producers continue to struggle with cattle numbers, resulting in higher livestock pricing than expected. This is impacting throughput, with a reduction of steers of around -3% through July (-5% in June), causing GB cattle prices to move higher.

Increased demand for steaking items such as rumps and sirloins have pushed beef wholesale prices upwards for with suppliers securing these cuts ahead of last week’s barbeque demand over the bank holiday weekend. The latest data for the 12 weeks up to 4th August, saw beef volumes increase by 1.5% (1,800 tonnes) year on year. This was primarily driven by greater volumes of mince sold, a consistent consumer trend attributed to its versatility and lower price point.

Robust demand for beef products from both retail and foodservice sectors is likely supporting the deadweight cattle price. These higher prices may be bringing a few more cattle forward, with throughputs up both on the week and year.

Tip: Consider switching Beef to more cost-effective proteins such as Chicken or Pork. We also recommend adjusting menus to feature more cost-effective cuts of Beef.

PORK

EU grade S reference prices have eased in the latest week

Prices have been relatively stable for the last 5 months

EU pig meat production up 3% year on year, but demand remains subdued

Uncertainty has crept into the European market leading to more volatility.

Although European reference prices generally see more volatility than the UK, there has been minimal movement for several months. Average prices are behind those from last year by around 23p but remain historically elevated.

FRUIT & VEG

UK Crops: The continued wet weather is having an effect on crops such as leafy salads and some berries as we are now starting to see more incidences of moulds and mildews in the field. Due to the high water content, crops are also a more delicate and prone to bruising after harvest.

The early Potato harvest has begun, with yields slightly below last year’s levels. Quality is variable, with typical early-season issues expected, such as loose skins and green tops.

This year, there may be availability challenges for small potatoes due to increased demand outpacing supply. The full impact on the season won’t be clear until November, once most of the crop has been harvested and quality can be thoroughly assessed.

A mix of frost and heavy rains in South Africa has negatively impacted yields of Oranges, Lemons and Easy Peelers, leading to a challenging market in the coming weeks.

Following early-season heat, poor Melon yields are anticipated in Spain, making for a challenging end to the season, particularly for Watermelons. There are also concerns around Galia and Cantaloupe varieties.

Get ready for the first crop of heritage carrots this month arriving in purple, white and yellow varieties, these striking roots will set the plate ablaze with colour and flavour.

Tip: Consider Carrots, Cauliflower and Butternut Squash instead of Potatoes. Limes can be used instead of Lemons as these are not currently being affected.

Cherry season has come to an end so beware of imported prices increasing.

UK quince are growing in popularity and will start to appear around mid-month. The apple-shaped pear is perfect for making and stocking up on jellies, preserves or pastes for the months ahead.

Tip: Damsons are a great option this month if you are looking for something quirky. The small plum-like fruit has many culinary uses including desserts, preserves or even in gin or vodka-based cocktails.

We are entering into the early stages of a crucial transition period for European Salads from UK and Northern European Summer Crops over to Mediterranean winter produce. Currently, Spanish growers have no concerns over Tomatoes, Peppers and Cucumber crops for the coming season. UK and Dutch produce will remain available until towards the end of October although there will be small pockets of Spanish appearing at the end of this month. Historically we know there can be challenges in the coming months. These can be cause by cooler growing conditions forcing UK and Dutch crops to finish earlier than expected. UK whole-head salad will continue throughout the month with the switch over to Southern European produce in late Sept / early Oct.

AT THEIR BEST:

Blueberries

Heritages Carrots

UK Beetroots

UK Damsons

UK Summer Squash

Turkish Figs

PLANNING AHEAD:

Main Crop Potatoes

UK Quince

Pumpkins

Chards

POULTRY

In the UK, there is a growing demand for poultry produced under higher welfare standards, which emphasizes lower stocking densities and longer lifespans for birds. While these standards improve animal welfare, they also result in reduced overall supply, as fewer birds are available throughout the year. This shift in production practices is likely to contribute to tighter supply conditions in the UK market.

EU Poultry prices have remained stable; however supply is currently challenging and placing pressure on price, driven by the following key factors:

The EU has introduced a cap on Ukrainian poultry imports, significantly impacting supply. This measure, aimed at protecting the EU poultry industry from low-cost Ukrainian imports, reduces the cap to 137,040 m/t – a 40% decrease YoY.

UK Border health controls for animal-origin products have increased certification costs, adding administrative burdens, causing delays at the border. This is making EU markets more appealing than the UK market.

Feed costs are expected to increase slightly in the next few months due to turmoil in the Middle East and weather-related risks in Russia.

The Turkey market is anticipated to face sharp price increases in the coming months. Smithfield's exit from turkey production to focus on poultry meeting the European Chicken Commitment (ECC) standards in the below section has led to a significant reduction in supply, cutting availability by 30,000 birds per week. This reduction, combined with limited frozen stock in cold stores across Europe, suggests a potential shortage as the festive season approaches. The situation could be exacerbated by any bird flu outbreaks, further driving up prices and limiting supply.

UK KEY MARKET MOVERS (CPI)

The Consumer Prices Index (CPI) is a key measure of inflation in the UK. Movements in CPI give a high-level overview of the key categories experiencing inflation. Below is a monthly snapshot of the top food commodity price inflation movements impacting the UK. The data is from Office for National Statistics (ONS).

Percentage change over 12 months:

Milk, cheese and eggs: -0.2%

Oils and fats: 9.2%

Breads & cereals: 0.2%

Vegetables: 2.1%

Meat: 0.7%

Sugar, jam, syrups, chocolate and confectionery: 5.1%

Fish: -4.2%

Fruit: 2.7%

FINAL WORD

Regency continue to proactively mitigate availability issues and supply risk, putting solutions in place to reduce impact, such as product switches and recipe re-engineering.

When analysing the affects that inflation has on your businesses purchasing, it's important to understand that inflation affects not only the price of goods, but also the quality and availability - this is something that our team of procurement experts can assess in detail, to ensure our members are always achieving the best outcomes in all areas. To find out more about ways in which we can help save your business time and money, get in touch.

We use cookies to ensure you get the best experience on our website. Learn more

Stay connected

Enter your email address to be kept up to date with latest news, company developments and market insights. You can unsubscribe at any time.

View our Privacy Policy.