Inflation outlook and foodservice market update - February 2026

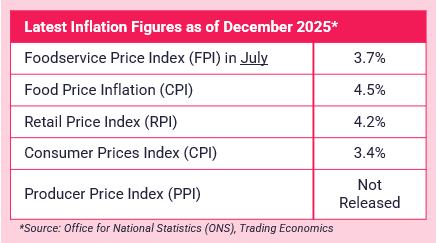

The Consumer Prices Index (CPI) rose by 3.4% in the 12 months to December 2025 up from 3.2% in the 12 months to November. Food and non-alcoholic beverages prices rose by 4.5% in the 12 months to December 2025, up from 4.2% in the 12 months to November. On a monthly basis, food and non-alcoholic beverages prices rose by 0.8% in December 2025, compared with a rise of 0.5% a year ago.

Market movers:

UK KEY MARKET MOVERS (CPI) The Consumer Prices Index (CPI) is a key measure of inflation in the UK. Movements in CPI give a high-level overview of the key categories experiencing inflation. Below is a monthly snapshot of the top food commodity price inflation movements impacting the UK. The data is from the Office for National Statistics (ONS). Percentage change over 12 months: FINAL WORD Regency continue to proactively mitigate availability issues and supply risk, putting solutions in place to reduce impact, such as product switches and recipe re-engineering. When analysing the effects that inflation has on your businesses purchasing, it's important to understand that inflation affects not only the price of goods, but also the quality and availability - this is something that our team of procurement experts can assess in detail, to ensure our members are always achieving the best outcomes in all areas. Equally, we fully understand the challenges presented by the increase in Employer National Insurance Contributions and National Living Wage, along with reduction in business rates relief and increased water bills. Our team of experts are working closer than ever with our members to reduce their purchasing costs in attempt to lessen the impact of rising costs in other areas of the business. To find out more about ways in which we can help save your business time and money, get in touch. Sources: Foodbuy, Fairfax Meadow, Birtwistles.

Search