Inflation outlook and foodservice market update - March 2026

26 March, 2026

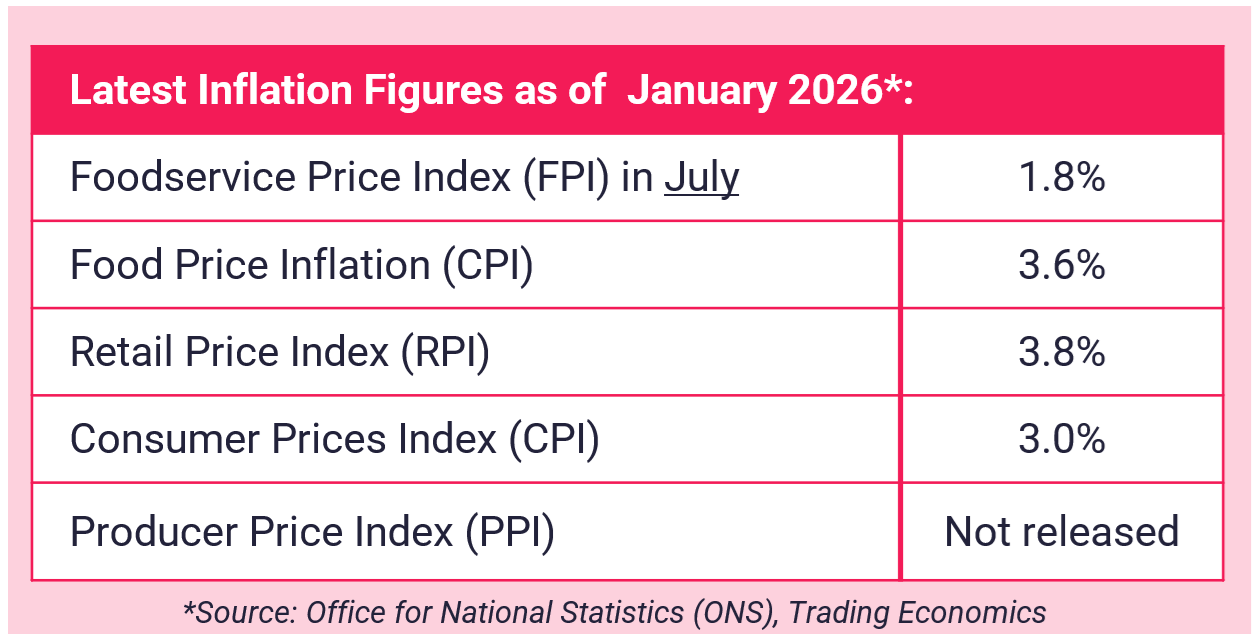

The Consumer Prices Index (CPI) rose by 3.0% in the 12 months to January 2026, down from 3.4% in the 12 months to December 2025. Food and non-alcoholic beverages prices rose by 3.6% in the 12 months to January 2026, down from 4.5% in the 12 months to December 2025. The Retail Price Index (RPI) is now 3.8% vs 4.2% last month down 0.4%.

Market movers:

FISH & SEAFOOD

Salmon: Prices have remained high in recent months, driven by reduced harvesting over the Christmas period. Typically, we would now see prices peak and begin to soften into Spring. However, prices continue to rise, and a short-term decrease looks unlikely.

Mackerel: Prices have softened, but volatility remains high. Further landing cuts of up to 75% are being proposed, in addition to the existing 22% reduction, reflecting stock pressures. Limited fishing activity is keeping line-caught fish at a premium. Currently rated MCS 3 (hook and line), all mackerel is now under review due to declining stocks.

White Fish: Strong demand is driving continued price increases across the market. Cod and haddock remain on an upward trend, and with reduced Barents Sea quotas, prices are unlikely to ease in the coming months.

TOP TIP: Coley: While prices have risen in response to wider white fish inflation, coley remains a strong value option and a good alternative to more expensive species.

DAIRY

Mozzarella has increased by 15% since the start of February. It currently has the highest market value when compared to similar cheeses. Supply remains relatively tight, which has been the main cause of these increases. However, a significant shift in production could quickly place downward pressure on prices.

Cream: Oversupply across the UK and Europe continues to keep prices suppressed. Currently undervalued versus butter, cream is expected to firm as the market rebalances. Herd reductions, driven in part by strong beef prices, are set to reduce output and apply upward pressure to milk prices.

MEAT

Beef: Tight cattle supply remains the key issue for 2026. Despite a brief easing earlier in the year, availability is still constrained. Strong forequarter demand is driving up prices for mince and burgers, while softer premium cut demand may offer some balance.

Lamb: Seasonal pricing patterns have shifted due to Southern Hemisphere supply, while UK flock numbers sit at record lows. Tight availability has persisted from Q1–Q3, with weather and lower production already impacting supply. Prices are expected to remain challenging throughout 2026.

Pork: Prices have held steady in 2026, driven by improved yields and restricted exports to China. Continued stability could open the door to price reductions. However, African swine fever remains a concern across Europe, although infections in domestic pig are still below 2024–2025 levels.

TOP TIP: Pork continues to offer stability in both availability and pricing. With cost pressures affecting most other animal proteins, pork presents a cost-effective alternative where suitable.

BAKERY

Cocoa (West Africa & Belgium): Production recovery in West Africa is emerging, but Ghana’s 50,000-tonne stockpile continues to weigh on the market. Prices remain in a long-term downtrend, recently falling below key moving averages. Forecasts point to a potential 65% decline into Q3 2026 (currently c. GBP 3,000/MT), subject to supply developments.

Wheat: Prices remain soft ahead of a seasonal low into May. Any decline is expected to be short-lived, with Mintec forecasts pointing to stability or slight easing before renewed inflation into Q3 and late 2026.

GROCERY

Cocoa: Prices in early 2026 have eased back to 2023 levels, following record highs in 2024 and early 2025 driven by poor yields and extreme weather. The current downward trend reflects a shift from supply deficit to projected surplus, alongside softer demand after last year’s price spike. Despite this, the market remains cautious, with varying origin supply and ongoing volatility risks.

NON-FOOD (SES)

Middle East Conflict: Ongoing tensions are expected to drive oil price volatility, increasing production and transport costs for non-food items such as packaging and chemicals. While suppliers have not yet implemented surcharges, a prolonged conflict could see energy charges reintroduced, similar to those following the Russia–Ukraine crisis.

FRUIT & VEG

Shipping Delays: Ongoing weather disruption is driving delays and congestion across global shipping routes. Some vessels are skipping UK ports entirely, offloading in Europe and creating additional delays as produce is transported back into the UK.

Limes: Delays to Brazilian shipments are causing widespread shortages across the UK and Europe. Diverted vessels are supplying mainland Europe, but the UK is seeing limited availability. With multiple shipments affected, disruption is expected to continue for at least two weeks, and global alternatives remain scarce.

Lettuce - There has been some improvement with better weather supporting crop growth and helping growers load produce. However, the market remains challenging and there could be some further issues in March, as planting schedules were disrupted by storms.

Lemon - At the start of the Spanish season, we anticipated late season tightening due to low yields. Recent heavy rainfall has reduced availability of smaller lemons even more, and this pressure is expected to continue into March.

Savoy cabbage suffered frost damage earlier in the season, requiring heavier leaf trimming and resulting in lower finished weights.

Peppers continue to face significant challenges. Low temperatures are restricting production, and the peppers available continue to show humidity related quality defects.

Avocados - Supply of avocados is challenging and may affect availability in the coming weeks. Industrial action at Israeli ports has slowed outbound shipments, while weather issues in Spain and Morocco have affected both crop development and transportation.

British apples - We are coming towards the end of our seasonal British apples line. Stock is expected to last for another couple of weeks, before the season finishes

TOP TIP: With shipping delays affecting fresh produce, we recommend prioritising British, in-season lines. Current options include potatoes, carrots, leeks, fennel, spring greens, rhubarb, celeriac, parsnips, swede, and purple sprouting broccoli.

UK KEY MARKET MOVERS (CPI)

The Consumer Prices Index (CPI) is a key measure of inflation in the UK. Movements in CPI give a high-level overview of the key categories experiencing inflation. Below is a monthly snapshot of the top food commodity price inflation movements impacting the UK. The data is from the Office for National Statistics (ONS).

Percentage change over 12 months:

Milk, cheese and eggs: 1.3%

Oils and fats: -1%

Breads & cereals: 1.5%

Vegetables: 2.3%

Meat: 5.2%

Sugar, jam, syrups, chocolate and confectionery: 10.4%

Fish: 1.2%

Fruit: 2.4%

FINAL WORD

Regency continue to proactively mitigate availability issues and supply risk, putting solutions in place to reduce impact, such as product switches and recipe re-engineering.

As you are likely aware, the situation in the Middle East is evolving rapidly and has the potential to affect global trade.

When analysing the effects that inflation has on your businesses purchasing, it's important to understand that inflation affects not only the price of goods, but also the quality and availability - this is something that our team of procurement experts can assess in detail, to ensure our members are always achieving the best outcomes in all areas.

We want to reassure you that the majority of our food products are sourced from the UK and EU, and at this time, there is no disruption to our supply chain.

We are closely monitoring developments and remain in regular contact with all our suppliers and brand owners to assess any potential impacts, particularly on imported products, which are mainly non-food items. So far, the only category directly affected is crude oil...

Rising oil prices are influencing transportation costs, manufacturing energy and packaging materials. This may also gradually affect certain products, including cooking oils and oil-rich items like mayonnaise, non-food plastics such as bin liners and food packaging and fish. We’re proactively reviewing our strategies to manage these impacts and maintain supply continuity. Please be assured that robust contingency plans are in place, and we will continue to provide Regency members with timely updates as the situation develops.

To find out more about ways in which we can help save your business time and money, get in touch.

Sources: Foodbuy, Fairfax Meadow, Birtwistles.

We use cookies to ensure you get the best experience on our website. Learn more

Stay connected

Enter your email address to be kept up to date with latest news, company developments and market insights. You can unsubscribe at any time.

View our Privacy Policy.