Inflation report - Recap on the last quarter and next quarter outlook

20 November, 2025

Recap on the last quarter

The last quarter has seen the CPI inflation measure in the UK rise from 2.0% in December 2024 to 2.8% in February 2025.

Overall the market was more volatile in the last quarter than in previous months. The heavy rain and flooding in parts of Spain continued to affect Fruit and Vegetable pricing. Cattle numbers were down by 5%, and the USA tariffs on Chinese trade have started to further drive up Seafood prices.

Market movers:

FRUIT & VEG

Pests – This summer has been the driest in almost 20 years, posing significant challenges for growers. Due to the extreme weather conditions, we have seen a rise in the influx of insects, as our watered and well-maintained crops provide an ideal environment for these insects to thrive. Additionally, until the arrival of the recent rains, growers have been unable to effectively treat plants as they need water to transport the treatment around the plant. Without water, the treatment is ineffective.

Brassica and Lettuce have been the most affected by the pests although growers have been working hard to minimise the impact. They have stripped back leaves to remove pests, checking the crops before harvesting and leaving any areas of severe infestation in the ground, reported to be 50% in some areas. With some varieties of lettuce such as Iceberg, as it grows from the inside out, we have seen aphids contaminate the immature heads and become enclosed as the plant grows around them. This means that contact treatment cannot penetrate to the inner layers and take effect, which is adding to the problems.

Cabbage – The availability of both red and white cabbage has been significantly impacted by the heat and lack of water during summer. These extreme conditions affected the main growing period, leading to a reduction in yield. There are also some continuing quality issues, caused by insect damage and edema, which means that more leaves need to be cleared away to reach acceptable quality, reducing head weight and yields.

Potatoes – Due to the hot spring and summer, we are seeing an increase in dry matter on potatoes, which is leading to more internal bruising. The dry weather is likely to create some challenges for larger potatoes, especially larger bakers which could result in less availability further along the season. We will not know the final impact until after the full harvest in November.

IMPULSE

We have seen significant inflation this year, with multiple double digit price movements across some of our Suppliers in this space. The main driver has been the surge in cocoa prices, which have reached USD 11,000 per tonne, compared to a historical average of around USD 2,200 per tonne prior to 2024. While future market movements remain uncertain, we recommend clients continue to review retail selling prices to ensure they’re in line with market guidance and competitor pricing (especially supermarket benchmarks).

GROCERY

Chopped Tomatoes & Puree – At the start of the summer harvest, prices were initially high due to challenging weather conditions in Italy, one of the main producing countries, which experienced unusually heavy rainfall and higher temperatures than in previous years. This led to some early volatility in the market before prices eventually stabilised back to last year’s levels.

Canned Fruit – Over the past 12 months, Peach production has been heavily impacted by volatile weather conditions, from spring hail and frost to summer heat. This has led to an increase in deformed fruit as mites spread more easily in the warmer climate. As a result, this year’s crop yield is down by approximately 25%.

Pineapple - Hot weather in spring 2025 reduced crop yields, while a backlog of orders has kept supply tight despite steady demand. Overall supply is down 41% compared to the 15-year average.

DAIRY

Milk - Between July and September, milk production rose 3.6% compared to the same period last year. This increase was mainly driven by lower feed costs, which encouraged farmers to boost milk output. Organic dairy milk has remained strong, largely due to a continued shortage of organic milk in the market.

Butter - Prices have remained stable, though still at elevated levels. This has been supported by weaker supplies across the continent, which is helping to boost export demand.

MEAT

Beef - After a record year for beef inflation, pricing is beginning to stabilise in the market. Over the past quarter, prices have risen by around 1.7% since July, with variation depending on the cut. Primal cuts have been relatively stable, while the cheaper and processed products have seen sustained pricing pressure as consumer demand has shifted to the cheaper cuts, as they look to respond to the record high prices. The market is up approximately 26% year-on-year (October 2024 to October 2025).

Chicken -This year has seen significant inflation in chicken prices, with increases of approximately 18–22% across both the UK and EU markets since the start of the year. Avian influenza (AI) outbreaks earlier in the year and improved stocking density requirements have led to a decrease in availability, increasing prices. UK Red Tractor-certified stock is particularly scarce at present. Inflation in the previous quarter was around 8-12% on chicken.

Turkey - Over the last eight months, UK whole turkey prices have risen by an average of 25–28%, driven by severe supply chain disruptions. Widespread AI outbreaks across the UK and Europe have forced culls, reduced breeder stock, and disrupted imports from key suppliers such as Poland, France, and Hungary. We’ve seen increases of approximately 10-15% in the previous quarter.

Pork - Pricing remained stable during the previous quarter, making it one of the most cost-effective protein options currently available.

Next quarter outlook

MEAT

Beef - Indicators suggest that further inflation on beef in the next quarter is likely. Cattle and kill numbers are down and demand remains strong. Deadweight pricing is approaching £6.50 per kg, and we anticipate it to be above this level before the end of the year. Christmas historically leads to an increase in demand for beef, most likely adding further demand pressures to an already constrained market.

Chicken -We anticipate further inflation this quarter. Demand remains high for chicken in the UK, imports from Europe still haven’t recovered to previous levels and this is putting pressure on UK producers. UK Red Tractor assured stock is particularly scarce. We’re entering prime Avian Influenza (AI) season as we move into winter months, any outbreaks could have a major impact on availability and, in turn, pricing.

Turkey - Last year, fresh turkey prices rose by approximately 20-30% in the lead-up to Christmas, and a similar trend is expected this season. In contrast, frozen turkey pricing tends to remain more stable during this period. We’ve had reports that one of the largest importers into the UK has temporarily suspended imports, due to an outbreak of Newcastle disease being detected within four miles of its processing plant. Imports have been halted for a minimum of 30 days, adding further pressure to an already tight supply situation.

Pork - We don’t anticipate any challenges or inflation with pork during the next quarter.

Turkey - We recommend focusing on frozen turkey if you are looking to shield yourself from inflation on fresh turkey in the run up to Christmas.

DAIRY

Looking ahead to the next quarter, the recent autumn rainfall following the drought has led to a flush of grass growth. This could ease pressure on forage stocks for now and might even allow for a late silage cut. However, forage availability and costs are still expected to be a challenge for some farmers this winter.

With high levels of Milk production, there’s growing pressure on processors to manage the surplus. If this excess supply isn’t absorbed, it could lead to downward pressure on farmgate prices to curb production.

Additionally, the milking herd is starting to shrink, largely due to high beef prices and ongoing labour shortages. If this trend continues, we may see a decline in milk production over the coming year.

There’s some hope that the current high milk production can be redirected into Butter, which could help ease prices going forward.

FRUIT & VEG

As we enter the winter months, root vegetables are back in season, while salad and berries are out of season. We recommend chefs build their menus around in-season products such as Carrots, Onions, Potatoes, Parsnips and Squash.

Potatoes – We expect the effects of the hot and dry growing season to continue. Higher dry matter levels are likely to persist, and availability of larger potatoes, particularly bakers, may tighten once the full harvest is complete in November. We will be monitoring quality and supply closely as results come in.

Lettuce - We expect lettuce supply to transition from British to Spanish as we move into the next quarter. Pest pressure has eased, but weather conditions in Spain may continue to affect availability and quality in the short term.

Broccoli - Spanish broccoli is likely to become the main source of supply. While availability should remain good, pest pressures and weather conditions in Spain may affect quality and consistency. Suppliers will continue working closely with growers to manage these challenges.

Cabbage - Pests are likely to continue affecting cabbage varieties, including Savoy and Cavolo Nero, with whitefly and other insects potentially impacting crops. Maintaining weight may remain a challenge, and concessions could continue to be necessary.

Lemons - Supply is expected to transition to Spanish lemons. While the Spanish harvest is likely to be smaller than usual, quality and size are expected to remain good.

FISH & SEAFOOD

Salmon - As we enter the colder months, salmon prices are expected to rise. Slower growth rates and the onset of winter sores are reducing the availability of larger, premium-quality fish, putting upward pressure across all salmon categories. Processors and smokers have already anticipated this trend, with price increases beginning to appear across the board. This pressure is likely to intensify in the run-up to Christmas.

Chalk Stream Trout - Offers strong commercial and sustainable value, making it an excellent alternative to farmed salmon as we approach December.

Whitefish - Cod remains a key concern, with prices at their highest levels in several years. Quotas continue to be reduced, and the upcoming Total Allowable Catch (TAC) is expected to fall by another 20% - the fourth consecutive year of cuts. Haddock, the natural alternative, is also seeing upward price pressure despite increased quotas in the Barents Sea. Supply is available, but affordability remains a challenge as demand shifts from cod to haddock.

For viable alternatives, fresh Hake presents a premium option, while Alaska Pollock stands out as the most cost-effective and sustainable choice (MCS rating 1*) for core menu items.

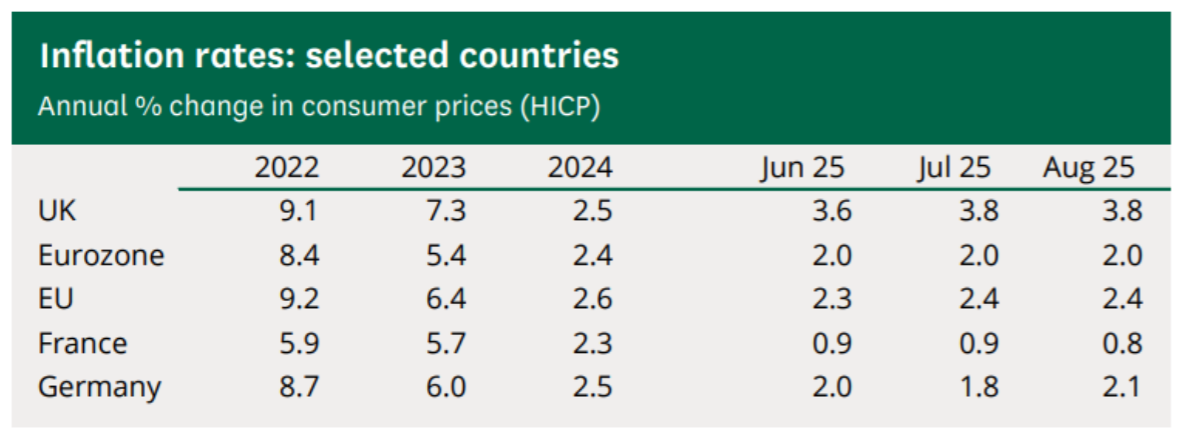

Labour driving underlying inflation

As shown earlier in this report, commodities continue to experience inflation driven by true commodity movements — i.e., supply tightening as demand increases, or vice versa. However, in the UK, we are seeing Total Consumer Price Index (CPI) and Food CPI grow faster than commodity inflation. This is being driven by government-led labour cost increases, such as the rise in the National Living Wage (NLW) and increases in National Insurance (NI).

Since April 2025, when these increases took effect, we have seen these costs gradually filter into the supply chain. Businesses have been weighing whether they can pass these costs on or absorb them. As cost pressures have continued to build, businesses now have little choice, and this impact is emerging as the main driver of increased supply chain costs.

This is clearly illustrated in the graph below: Europe is experiencing traditional commodity-driven inflation rates, whereas UK rates are elevated, reflecting the impact of NI and NLW on supply chain costs.

We expect this trend to continue over the next six months, with CPI and, more importantly, Food CPI, remaining elevated compared with Europe. If the government does not introduce further increases, we could see CPI and supply chain costs soften in the spring, rising only around 2–3% rather than the current elevated level of 5% for Food CPI.

We use cookies to ensure you get the best experience on our website. Learn more

Stay connected

Enter your email address to be kept up to date with latest news, company developments and market insights. You can unsubscribe at any time.

View our Privacy Policy.