Inflation outlook and foodservice market update - May/June

5 June, 2026

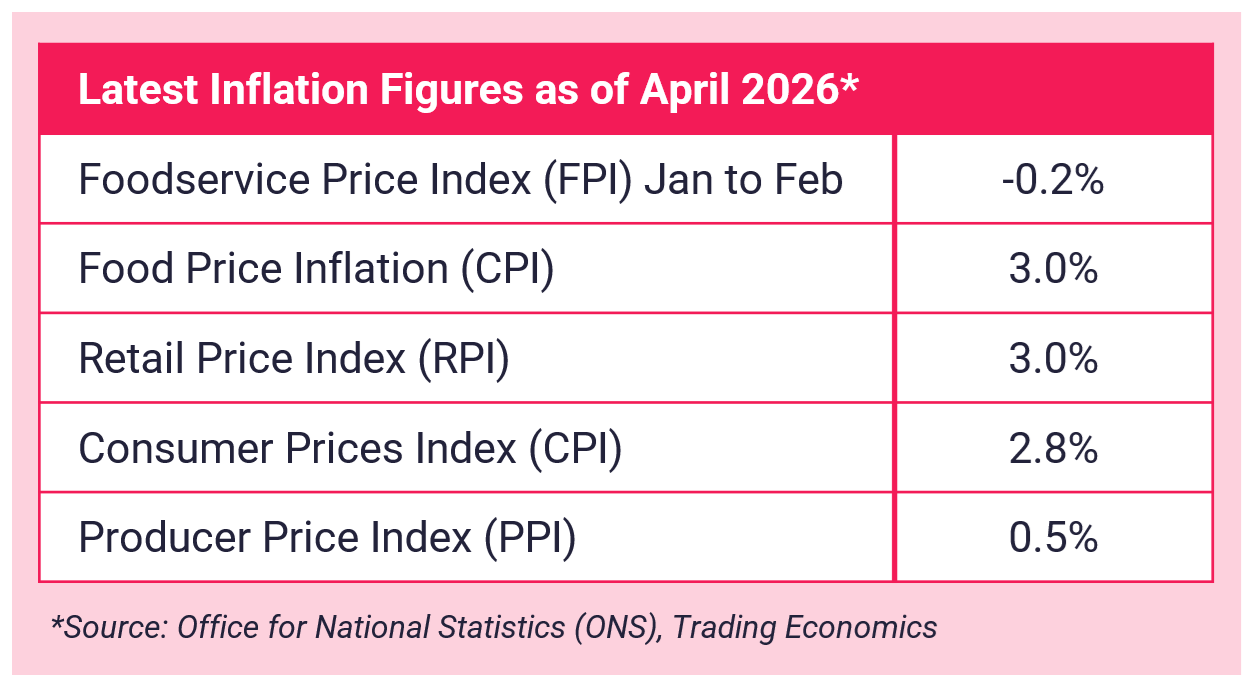

The Consumer Prices Index (CPI) rose 2.8% in the 12 months to April 2026, down from 3.3% in the 12 months to March.

The annual inflation rate for food and non-alcoholic beverages was driven lower by price movements in five of the 11 categories: meat; sugar, jam, honey, chocolate and confectionery; oils and fats; coffee, tea and cocoa; and mineral waters, soft drinks and juices. These declines were partly offset by upward pressure from vegetables and from milk, cheese and eggs.

On a monthly basis, food and non-alcoholic beverage prices were little changed in April 2026 but rose by 0.7% a year ago.

Market movers:

MEAT

Lamb: UK lamb prices remain at exceptionally high levels, driven by tight supply following adverse weather in 2025, which reduced flock numbers and limited market availability. Higher production costs have added further upward pressure. Prices eased slightly as new-season lambs entered the market, but upward pressure is expected to re-emerge in Q3. With limited import availability from Europe and the Southern Hemisphere, prices are likely to remain elevated throughout the summer.

Chicken: Strong consumer demand continues to support the UK poultry market, with consumption growth outperforming other proteins. Tight supply, lower stocking densities and higher feed costs have driven modest price increases in 2026. EU imports have declined as a stronger euro and Avian Influenza restrictions have reduced their competitiveness, adding further pressure to UK supply.

Pork: Pork continues to offer stability in both availability and pricing. With cost pressures affecting most other animal proteins, pork presents a cost-effective alternative where suitable.

DAIRY

After a long period of favourable dairy pricing, the UK dairy market is beginning to tighten, with May bringing increasing upward pressure on raw milk costs. Commodity markets strengthened during the first quarter of 2026, and several processors have now announced price increases for May. Arla increased its milk price by 1.79ppl, while Barbers Cheese confirmed a 1.55ppl rise. Overall, the market appears to be trending upwards again.

FISH & SEAFOOD

Salmon: Salmon prices have fallen sharply this month as increased supply into European markets has eased short-term pressure, although the market remains volatile with limited biomass growth still posing a supply risk longer term.

Sea Bass & Bream: Farmed sea bass prices have eased, while bream remains broadly stable. Market conditions are expected to remain relatively balanced, although future supply remains dependent on stock recruitment following last summer’s poor growing conditions.

Whitefish: Cod prices have softened slightly short-term, however the long-term outlook remains inflationary due to significant quota reductions impacting both fresh and frozen supply. Haddock prices have also eased seasonally, while hake has risen sharply due to limited availability and increased substitution.

Other Species: Halibut prices have eased, particularly for larger fish sizes, while increased seasonal landings have driven monkfish prices lower. Mackerel remains volatile, with sustainability concerns continuing to impact sourcing decisions.

FRUIT & VEG

Blueberries: The UK crop remains around two months away, while Moroccan output is declining, resulting in significant supply shortages.

Lemons: Smaller sizes will remain difficult to secure until June as we await the Eastern Crop from South Africa.

Melons: Supply remains tight during the handover from Central American to Spanish production, with Honeydew particularly affected as the Spanish season gets underway.

Savoy Cabbage: The UK season ended earlier than expected, resulting in supply shortages. Availability is also constrained across Spain and wider Europe, while quality issues affecting imported product have led to smaller head sizes.

Peppers: Spain and Morocco still have extremely limited supply. Sweet pointed peppers are also limited due to the lack of volume from Holland which is keeping prices elevated.

Lettuce & Leaves: Pak Choi availability remains tight following insect damage to UK crops, which has reduced yields. Spinach supply from Spain and Portugal remains strong, although high temperatures and tired fields are increasing the risk of insect pressure and yellowing.

Onions: Quality issues continue to affect both brown and red onions. Over the next two weeks, the extent of the impact on stored brown onion stocks should become clearer, with the potential for further challenges later in the season. Risk remains elevated for red onions until the transition to new-season Egyptian supply, expected in the third week of May.

Sweet Potato: Very limited availability expected for the next two months due to the end of European season, significant US crop losses, and vessel delays.

Strawberries/Blackberries: Supply is almost entirely British for blackberries with this expected from strawberries within the next week. No issues with the supply forecasted.

Carrots: Scottish crop is harvesting well with good quality. Spanish crop is also developing well and in a good condition.

BAKERY

Cocoa: The cocoa market has continued to soften since March 2026, supported by improving West African production and reduced speculative activity, which has allowed us to chase deflation. While market sentiment remains sensitive to wider economic pressures, supplier pricing remains broadly stable.

Wheat: Wheat prices have continued to soften from the elevated levels seen in recent years, creating opportunities to pursue deflationary discussions where appropriate. Pricing is expected to remain relatively stable through Q2 and Q3 2026, although inflationary pressure could build from Q4 onwards if fertiliser shortages impact future planting cycles.

Sugar: Sugar prices remain relatively stable, albeit sensitive to global volatility. Pricing is stabilising and continues to follow a broader downward trajectory into May. European beet sugar remains particularly exposed due to the energy-intensive nature of processing, with pricing expected to show an upward bias during periods of oil price volatility. Overall, the market is forecast to remain broadly stable, with only minor fluctuations expected through 2027.

UK KEY MARKET MOVERS (CPI)

The Consumer Prices Index (CPI) is a key measure of inflation in the UK. Movements in CPI give a high-level overview of the key categories experiencing inflation. Below is a monthly snapshot of the top food commodity price inflation movements impacting the UK. The data is from the Office for National Statistics (ONS).

Percentage change over 12 months:

Milk, cheese and eggs: 2.0%

Oils and fats: -4.7%

Breads & cereals: 0.9%

Vegetables: 3.3%

Meat: 3.6%

Sugar, jam, syrups, chocolate and confectionery: 6.1%

Fish: 5.7%

Fruit: 3.1%

FINAL WORD

Regency continue to proactively mitigate availability issues and supply risk, putting solutions in place to reduce impact, such as product switches and recipe re-engineering.

As you are likely aware, the situation in the Middle East is evolving rapidly and has the potential to affect global trade.

When analysing the effects that inflation has on your businesses purchasing, it's important to understand that inflation affects not only the price of goods, but also the quality and availability - this is something that our team of procurement experts can assess in detail, to ensure our members are always achieving the best outcomes in all areas.

We want to reassure you that the majority of our food products are sourced from the UK and EU, and at this time, there is no disruption to our supply chain.

We are closely monitoring developments and remain in regular contact with all our suppliers and brand owners to assess any potential impacts, particularly on imported products, which are mainly non-food items. So far, the only category directly affected is crude oil...

Rising oil prices are influencing transportation costs, manufacturing energy and packaging materials. This may also gradually affect certain products, including cooking oils and oil-rich items like mayonnaise, non-food plastics such as bin liners and food packaging and fish. We’re proactively reviewing our strategies to manage these impacts and maintain supply continuity. Please be assured that robust contingency plans are in place, and we will continue to provide Regency members with timely updates as the situation develops.

To find out more about ways in which we can help save your business time and money, get in touch.

Sources: Foodbuy, Fairfax Meadow, Birtwistles.

We use cookies to ensure you get the best experience on our website. Learn more

Stay connected

Enter your email address to be kept up to date with latest news, company developments and market insights. You can unsubscribe at any time.

View our Privacy Policy.