Inflation outlook and foodservice market update - June/July

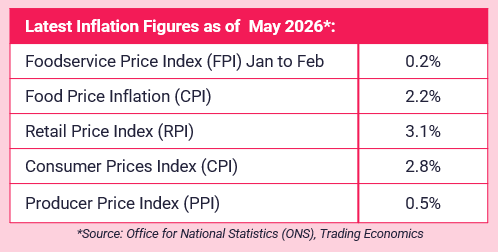

The Consumer Prices Index (CPI) rose 2.8% in the 12 months to April 2026, down from 3.3% in the 12 months to March.

The annual inflation rate for food and non-alcoholic beverages was driven lower by price movements in five of the 11 categories: meat; sugar, jam, honey, chocolate and confectionery; oils and fats; coffee, tea and cocoa; and mineral waters, soft drinks and juices. These declines were partly offset by upward pressure from vegetables and from milk, cheese and eggs.

On a monthly basis, food and non-alcoholic beverage prices were little changed in April 2026 but rose by 0.7% a year ago.

Market movers:

UK KEY MARKET MOVERS (CPI) The Consumer Prices Index (CPI) is a key measure of inflation in the UK. Movements in CPI give a high-level overview of the key categories experiencing inflation. Below is a monthly snapshot of the top food commodity price inflation movements impacting the UK. The data is from the Office for National Statistics (ONS). Percentage change over 12 months: FINAL WORD Regency continue to proactively mitigate availability issues and supply risk, putting solutions in place to reduce impact, such as product switches and recipe re-engineering. As you are likely aware, the situation in the Middle East is evolving rapidly and has the potential to affect global trade. When analysing the effects that inflation has on your businesses purchasing, it's important to understand that inflation affects not only the price of goods, but also the quality and availability - this is something that our team of procurement experts can assess in detail, to ensure our members are always achieving the best outcomes in all areas. We want to reassure you that the majority of our food products are sourced from the UK and EU, and at this time, there is no disruption to our supply chain. We are closely monitoring developments and remain in regular contact with all our suppliers and brand owners to assess any potential impacts, particularly on imported products, which are mainly non-food items. So far, the only category directly affected is crude oil... Rising oil prices are influencing transportation costs, manufacturing energy and packaging materials. This may also gradually affect certain products, including cooking oils and oil-rich items like mayonnaise, non-food plastics such as bin liners and food packaging and fish. We’re proactively reviewing our strategies to manage these impacts and maintain supply continuity. Please be assured that robust contingency plans are in place, and we will continue to provide Regency members with timely updates as the situation develops. To find out more about ways in which we can help save your business time and money, get in touch. Sources: Foodbuy, Fairfax Meadow, Birtwistles.

Search